Qualified Plan’s Response to Increase in Tax Liabilities

By now, a significant number of your clients have experienced the tax bite of ATRA 2012 with its increase in federal income tax rate from 35% to 39.6%, 20% capital gains tax, limits on itemized deductions, new 0.9% Medicare tax on earned income, and 3.8% Medicare tax on income streams previously not subject to this levy (e.g. rents, interest, royalties, etc.). See a detailed table here. However, their 2014 experience doesn’t have to retrace their 2013 tax return; a qualified retirement plan may provide a much-needed reprieve from the increased tax burden while complimenting your client’s total financial plan. A few proactive steps may help identify tax savings opportunities and create a road map to their effective utilization.

Breaking the Cycle

A retirement plan may prove to be one of the most effective tax management tools at small business owner’s disposal. There is a variety of plan alternatives, from IRA‐based plans (SEPs and SIMPLEs) to 401(k), 403(b), profit-sharing, and defined benefit plans. Each plan type carries a unique set of benefits, features, contribution limits, maintenance requirements, and set‐up deadlines.

For example, if a client is currently looking for a deduction to alleviate prior year’s tax burden, there is still time to start a SEP IRA; it is the only plan that may be established up to the due date of the employer’s tax return, including extensions. Contributions made in a timely manner will be deductible for the prior tax year. This makes SEPs a popular last-minute resort for those attempting to address prior-year tax liability. But is this reactive approach the best solution going forward? You can break the reactive cycle by investigating retirement savings plan alternatives.

A Case Study

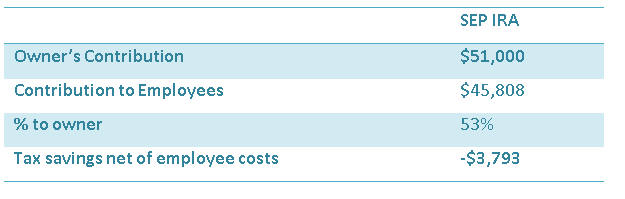

We recently compared several retirement plan options for a business that employs one owner and four employees. To obtain a deduction to help offset prior year’s tax liability, the only option available in the current year was a SEP IRA:

When analyzing the SEP opportunity, we found that the required employee deposit exceeded the owner’s tax benefit by nearly $3,800. In other words, from a pure net tax savings perspective, this client was better off not having a SEP IRA, and instead paying tax and investing on an after‐tax basis.

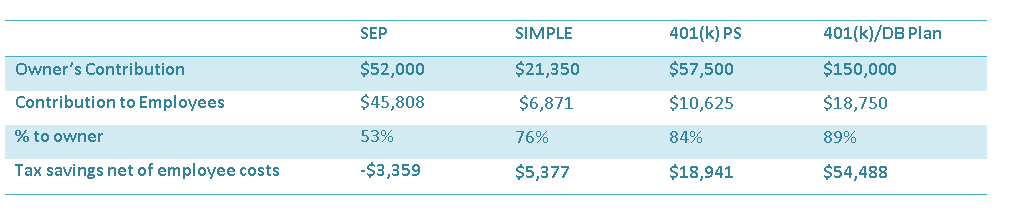

By evaluating the available current year plan options and projecting their tax impact, we were able to take pro‐active measures to address the individual’s tax liability and achieve attractive outcomes. Here are the results:

A SIMPLE IRA shows improvement in some areas, but is still far from an ideal result. The contribution for employees is significantly improved as compared to the SEP. As a result, the owner’s tax savings net of employee contribution costs is in positive territory. However, the contribution is simply too low for the owner to achieve his long‐term savings objectives and make a meaningful difference for his tax-savings goals.

A 401(k) profit-sharing plan offers a greater improvement by more the doubling the contribution opportunity ($57,500) for the owner as compared to the SIMPLE while only adding only about $3,800 to the required contribution for non-owner employees. The net tax savings is almost $19,000.

The final option, a combination of a 401(k) plan and a defined benefit plan, affords a contribution of up to $150,000 which yields a tax savings of over $54,000. In addition to expanded contribution opportunity, 401(k) and 401(k)/DB combo options contain provisions not available in IRA‐based plans:

• Access: Loans and in‐service distributions allow access to plan assets in a financial emergency.

• Tax-diversification: The Roth 401(k) feature creates an opportunity to build a tax-free bucket to offer tax diversification for future retirement income stream.

• Asset Protection: Finally, anti-alienation provisions of ERISA specifically protect the assets in the plan from judgment creditors.

By reviewing all options and taking a proactive approach, we are able to identify and optimal long-term solution that helps address a broad spectrum of needs of a business owner.

Questions to Ask

Begin your proactive planning process by asking your clients the following questions:

• How did your current retirement plan impact your tax picture?

• How satisfied are you with results?

• Does your retirement plan keep you on track to reach your retirement income needs?

• Does your plan maximize your tax savings today? Does it contain features to manage taxes in retirement?

• When was the last time you looked at the available alternatives?

We invite you to take the guesswork out this process. Work with Retirement Services to identify the available plan options, calculate each plan’s contribution potential, costs and net tax savings, and carefully understand what is required to establish and operate each plan. This will provide you with the information you need to make informed decisions, not only for the prior year, but also going forward. You can reach us at (888) 926-0600 or via email to pensions@firstallied.com .

You must be logged in to post a comment.