Taking the Guesswork Out of the SIMPLE v. 401(k) Decision

October 1 is an important deadline for SIMPLE IRAs and Safe Harbor 401(k) plans alike as it happens to be the last day of the year these plans may be established for the calendar year. By November 2, sponsors of SIMPLE IRA plans need to communicate to their employees company intentions for the plan in the upcoming year; this communication is accomplished through a mandatory Annual Participant Notice. With that, it’s important to evaluate which plan is the best fit in the current year and beyond.

While on the surface, SIMPLE IRAs are more attractive because they are fairly easy to establish and maintain, 401(k) plans typically offer considerably more flexibility in design, contribution range and access to funds, greater tax diversification, provide asset protection, and often help control staff costs better. The table below summarizes key characteristics and distinctions between these two plans:

SIMPLE IRA v. 401(k) Plan Case Study

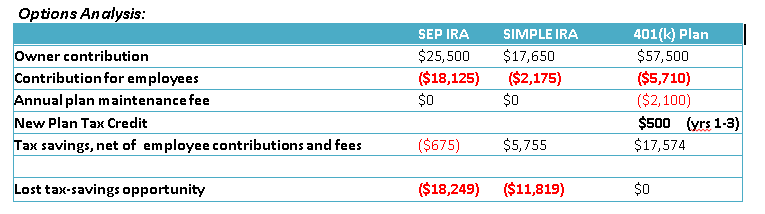

Recently, a small business owner in New York asked for assistance in evaluation of plan options for her company. We were asked to help determine whether a SEP, SIMPLE, or a 401(k) plan would help best meet client’s objectives. The table below illustrates the outcome of each funding scenarios net of employee and plan maintenance costs:

Facts:

• S-corporation

• Single owner with a W-2 of $102,000 per year; remainder of profit is treated as pass-through income on K-1

• Two eligible employees earning $32,500 and $40,000

• Objectives: maximize tax benefits for the owner

Bottom line: While SIMPLEs and SEPs offer a streamlined set-up, low maintenance, and minimum annual fees, the lost tax savings opportunity is very costly, $18,249(SEP) and $11,819 (SIMPLE) in the above examples, even after the administration costs associated with a 401(K) plan are taken in consideration. In addition, 401(k) plan option offers greater flexibility, tax-diversification options (ability to accumulate and later access assets on a tax-free and tax deferred basis), better manage employee benefit costs, and offer more robust asset protection.

We are Ready to Help

With the two important deadlines just around the corner, now is the time to start reviewing retirement plan options to identify optimal design, increase tax efficiency, and build retirement account balances. Retirement Solutions Consultants are prepared to assist you with:

1. Plan Design: review all available options and identify an optimum solution in light of all relevant facts;

2. Retirement Accumulation: find the savings vehicle that efficiently and effectively meets your objectives;

3. Tax Savings: work to reduce the unnecessary tax exposure through tax benefits inherent in qualified plans;

4. Investment Platform: review current platform for fees and services or help identify best options for a new plan.

Click here, call us at (888) 926-0600 send a message to retirement@firstallied.com

You must be logged in to post a comment.