Missed the Safe Harbor 401(k) Implementation Deadline? There is a Way

401(k) plans have some additional benefits and features when compared to simplified arrangements such as SEP or SIMPLE IRAs. For instance, they offer tax diversification by way of the Roth 401(k), a mechanism to convert balances to Roth (internal conversions), better accessibility to account accumulation in pre-retirement, and creditor protection under Title I of ERISA. If the employer elects to make a profit-sharing or a matching contribution, a vesting schedule can be attached to those funds enhancing the plan’s impact on employee retention.

Deferral and Match Tests

401(k) plans are required to perform testing in which the average deferral percentage (ADP) of the non-highly compensated employees (NHCEs) is compared to the average deferral percentage of highly compensated employees (HCEs). Too great a disparity requires a special contribution to NHCEs or reversal of a share of HCE contributions to bring the plan in balance. A similar test applies to matching contributions (ACP test).

A Safe Harbor Approach

To overcome this testing issue, retirement plans often utilize Safe Harbor provisions. Safe Harbor 401(k) plans require the employer to make either a 3% contribution for all eligible employees or a match for those who choose to defer. Safe Harbor 401(k)s automatically pass their ADP and ACP tests.

Implementation Deadline

Safe Harbor plans require that employees are offered a 60-day window to enroll. In addition, one needs a full month’s payroll after the enrollment window but before year-end to defer salary, making October 1 the last day for calendar-year businesses to establish a Safe Harbor 401(k).

Cure for a Missed Deadline

If a business owner desires to establish a 401(k) plan but missed the October 1 implementation deadline, he or she can still implement a traditional 401(k) without Safe Harbor provisions before December 1. A special rule available only for new 401(k) plans comes to the rescue. This rule allows the HCEs to defer 5% of salary and receive a match without concern over ADP or ACP test failure. The plan must be established before 12/1 and implement Safe Harbor provisions on January 1 of the New Year to take advantage of this opportunity.

Here’s how it worked for one of the companies we recently helped:

Facts:

• Consulting business established in Arizona

• S-corporation; two owners: husband and wife

• Four employees (three eligible in 2014)

• No plan

• Contribution objective: $60,000 – $80,000 plus employee contribution

Current Plan Year

Recommendation: establish a 401(k) plan with a discretionary match and profit-sharing.

Next Plan Year

Recommendation: The 5% rule is available only in the first year of a 401(k) plan; for that reason the plan needs to be amended to include a Safe Harbor match feature to protect the deferral and matching contribution opportunity for the highly compensated employees even if other participants choose not to make salary deferral contributions.

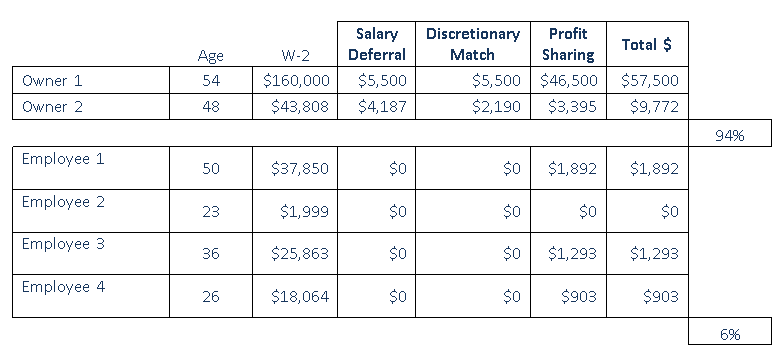

In the current year, the plan will allow the owners to save up to $62,272 with employee contribution of a little over four thousand dollars. Next year, with implementation of the Safe Harbor match provision, their contribution opportunity will increase to close to $80,000 with the required contribution for employees at about the same level as in the prior year.

Who May Benefit from This Approach

• Businesses that missed the safe harbor deadline but want to establish a 401(k) plan in the current year;

• Businesses with Profit Sharing Plans that would like to add a 401(k) feature in the current year;

• Businesses with a SEP IRA that are interested in exploring flexibility and efficiency available in a 401(k) plan program

Retirement Solutions Consultants are ready to help every step of the way, from discovery to proposal preparation and implementation. Call us at (888) 926-0600 or click here to connect with a consultant.

You must be logged in to post a comment.