Insulating Clients from Increased Tax Liability & Underfunded Retirement

When used in the same sentence, the words ‘change’ and ‘tax code’ are seldom associated with good news. Yet, every so often, changes in the tax code create opportunities for innovative design that take retirement plans to a whole new level. The Pension Protection Act (PPA) and subsequent regulations brought about new opportunities to effectively combine Defined Benefit Plans and Defined Contribution plans, building a compelling solution to help insulate clients from the risk underfunded retirement and increased tax burdens.

Background

Retirement plans fall into two basic categories: defined benefit and defined contribution. Defined benefit (DB) plans contain a promise of specific benefits upon retirement. Employers are responsible for funding defined benefit plans adequately, so the earned benefits can be paid to retirees. Defined contribution plans (DC), on the other hand, do not offer any guarantees. They are generally funded with employee salary deferrals and employer contributions and provide a lump sum payout made up from contributions and earnings.

For a company offering a defined benefit and a defined contribution plan, prior to the passing of the PPA, the maximum deductible employer contribution to all plans for a fiscal year was the greater of the required defined benefit plan contribution or 25% of participants’ eligible compensation. A paired plan would not increase the employer’s deduction.

The PPA changed the rules to allow employers to deduct contributions to a DC plan in addition to the required DB contribution, even if the resulting total exceeds 25% of participants’ eligible compensation. Subsequent regulations expanded and clarified how these plans may be designed and operated further increasing their appeal for closely held businesses.

Profile of an Ideal Combination Plan Prospect

Ideal candidates for such an arrangement are business owners who seek to save substantially more than a defined contribution plan, such a 401(k) or profit-sharing plan, would allow on its own. The business sponsoring a plan should be consistently profitable. The business owner should plan to work at least 3 years before retiring, and there should be a substantial difference in the owner’s age and income compared to the employees.

Building the Layers: Start with a 401(k)

401(k) provision allows eligible employees (including the owner) to defer a portion of their current compensation until retirement and receive immediate tax benefit while allowing the money to grow and compound on a tax-deferred basis.

For plans which cover non-owner employees, the employer will typically make a special Safe Harbor contribution to eligible participants. In doing so, the employer guarantees deferrals of the highly compensated employees do not violate 401(k) non-discrimination tests, helps fulfill the plan’s top-heavy requirements (most of small business plans are top heavy), and – in some cases – can count this contributions as a part of profit-sharing allocation used to satisfy the non-discrimination testing.

Add Profit Sharing

The remaining deduction is typically allocated to participants by way of a cross-tested profit-sharing plan. This plan design allows allocation of the bulk of the profit-sharing dollars to key contributors without violating non-discrimination requirements outlined by the IRS.

Top it off with a Defined Benefit plan

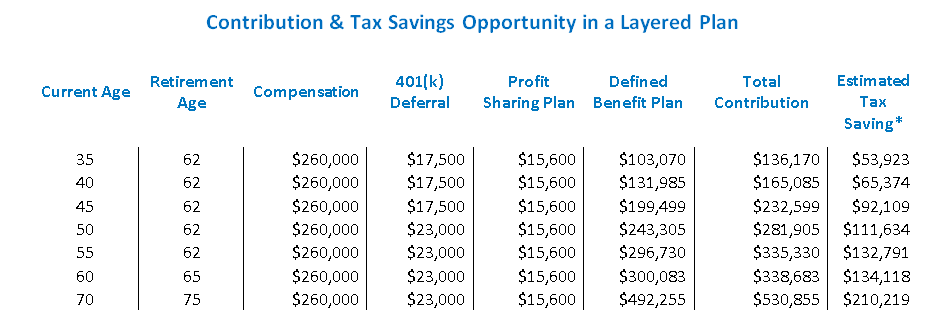

The final layer of a combination plan is the Defined Benefit plan or a Cash Balance Plan. Contributions to these plans require a complex calculation which encompass age, compensation, the length of time until retirement, the promised benefit, the assumed growth of plan assets, and a variety of actuarial factors. The annual funding requirement is recalculated each year to account for the actual performance of plan assets and any changes to the plan’s liabilities. In general, the more one makes, and the less time they have before retirement, the greater is the contribution required to fund that individual’s benefit under the plan. The end result is a robust plan that helps achieve tax reduction and retirement savings objectives. Here is a snapshot of contribution opportunities in a multi-layered retirement plan.

Timing for Setup and Funding

Generally, for a plan to be effective in the current year (or for another layer to be added), the plan document needs to be signed or amended by the last day of the employer’s tax year. For most small businesses, their tax year co-insides with the calendar year, making December 31 the deadline for current year plan implementation. Employer contributions, however, are not due until the following year. As long as they are deposited before the employer’s tax filing deadline, including extensions, they are deductible for the preceding tax year.

As you discuss year-end tax planning with your clients, consider introducing these concepts to them. Retirement Solutions Consultants are ready to help all the way.

Give us a call, (888) 926-0600, click to contact or send a message to retirement@firstallied.com.

You must be logged in to post a comment.