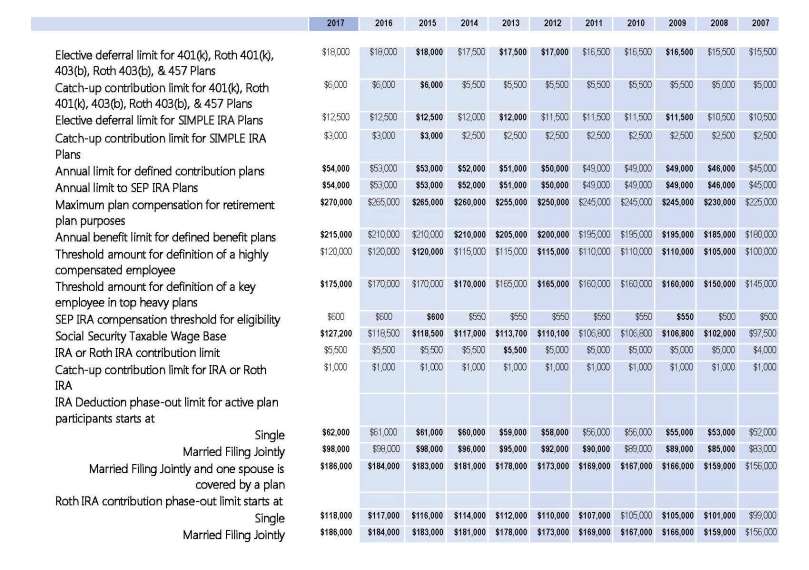

Cost of Living Adjustments Effective for Plan Years Beginning 1/1/2017*

On October 27, 2016, the Internal Revenue Service in Notice 2016-62 announced the cost-of-living adjustments that apply to dollar limits for retirement plans for the tax year beginning on January 1, 2017. As anticipated, since there was a modest increase in the cost of living, as measured by the Bureau of Labor Statistic’s Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) for the period covering the third quarter of 2014 to the third quarter of 2016, most of the retirement limits will remain unchanged. Salary deferral and IRA contribution limits, including catch-ups, remain at the 2016 levels; annual maximum contributions and defined benefit caps experienced a minor step-up.

In similar fashion, on October 18, the Social Security Administration announced a modest 0.3% cost of living adjustment to benefits; on the other hand, the Taxable Wage Base increased from $118,500 to $127,200. While the benefit adjustment limit is negligible, taxable wage base growth results in a $1,079 social security tax increase year-over-year for those with earned income at or above the limit.

NOTE: IRA deduction phase-out limits for Single, MFJ filers when one spouse is covered by a plan was increased by $1,000. A $1,000 increase in Roth IRA contribution phase-out was also extended to Single and MFJ filers. As before, we have highlighted the year-over-year changes for easy identification.

Click to view a year-over-year summary.

*This summary is designed to provide an overview of the dollar limitations for retirement plans applicable in 2017 and is not intended to be comprehensive. For a complete announcement of the applicable limits see IRS Notice 2016-62 and Social Security Administration’s 2017 Social Security Changes Fact Sheet.

This summary is for general information only and is believed to be accurate and reliable as of posting date but may be subject to change. Not investment, tax, or legal advice. Individuals should seek services from the appropriate tax and legal professionals as to applicability of this information in for their individual circumstances

You must be logged in to post a comment.